Proverbs 13:22: “A good man leaves an inheritance to his children’s children.” (NKJV)

Inheriting anything is such a blessing. I remember when my mother-in-law Debbie died suddenly how much of a blessing and a shock it was to my wife to inherit a little bit of money. Not much, mind you, but it was so much more than we were expecting. Knowing that someone loved you enough to save or set aside a little bit of something just for you is heartwarming. What an honor to receive such a gift!

I often work with people who are driven to a financial planner when they receive a gift from a deceased loved one. The grief is real, but there is almost always a fondness shared by the beneficiaries for the one who left them something behind. The question that naturally comes up after grief and gratitude is “How do I steward this gift wisely?” That’s what I’d like to answer today, specifically regarding Inherited IRAs.

IRAs are treated differently than many other gifts (I’ll write in more detail about capital gains and inheritance of “non-qualified” assets later). IRAs are tax-savings vehicles that incentivize people to save for retirement by promising a tax-break. You can have a brokerage account that is an IRA, a CD that is an IRA, an annuity that is an IRA, a money market account that is an IRA, a mutual fund account that is an IRA, and other forms of IRAs but the common denominator is that the IRS isn’t going to count contributions to that account (as long as they qualify) as income for the year you make them and you won’t be taxed on the growth/gains in that account until you take the money out (so long as you follow all the rules).

So what happens when you inherit an IRA?

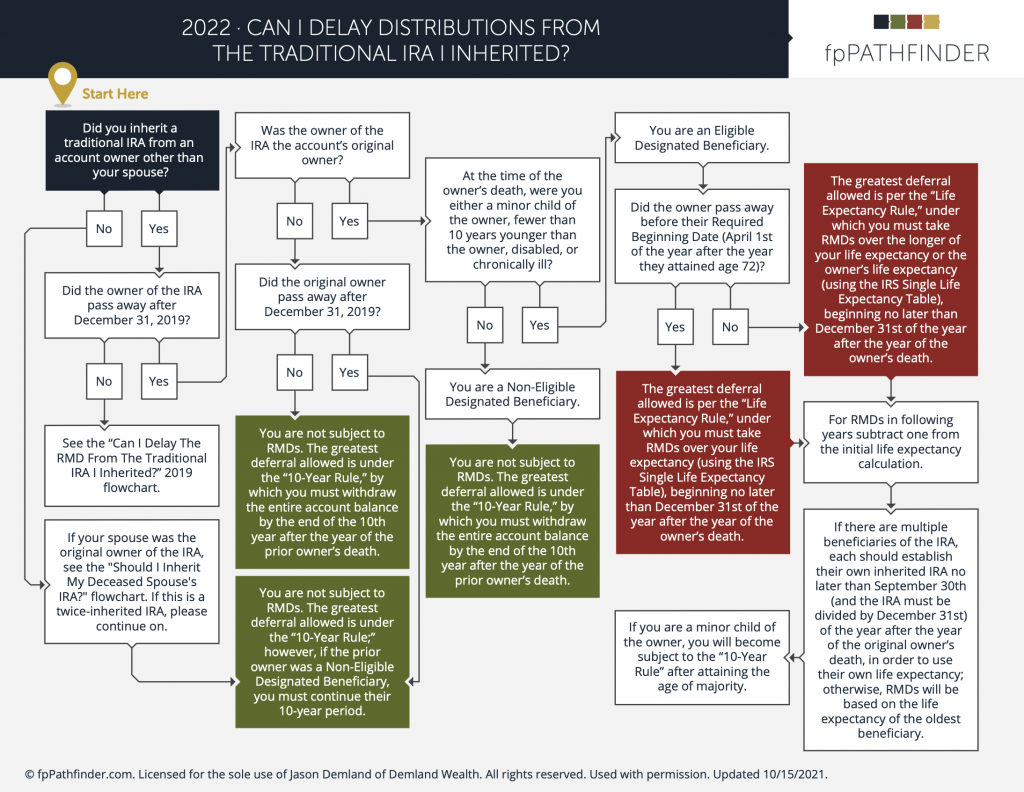

Recently there have been some changes made to how inherited IRAs work and many words have been written and many questions have been asked (and still are being asked) of the IRS about how this is all going to work out after the SECURE act passed in 2019. Usually unless you are an Eligible Designated Beneficiary your only option is to take out the entirety of your beneficiary IRA by the end of the 10th year after the year of the prior owner’s death. This is what is known as the 10 year rule. You can take it all out evenly, all at once, or wait until the end of the 10th year to take it out, but it must be emptied by the end of that 10th year. There is a small caveat in this rule, if the decedent died after their Required Beginning Date (when they needed to take RMDs) you may be able to use the old “stretch” provision. That’s pretty simple really, but figuring out which method will work best for your situation takes a lot more analysis. That’s because distributions from an inherited IRA will count as ordinary income and could cause you to fall into a higher tax bracket. It’s very important to have a plan to maximize your inheritance and keep the IRS from getting more than its fair share.

If you are an Eligible Designated Beneficiary (Surviving Spouse, Disabled, Chronically Ill, less than 10 years younger than the decedent, a minor child, and some “see-through” trusts) then you may be eligible to stretch the distributions out over your lifetime according to a table. This is sometimes more favorable than the 10 year rule and needs to be investigated thoroughly if it’s a possibility.

This has been just a short intro into what to do with an inherited IRA and a flow chart would be incredibly valuable in this scenario. Hey. I’ve got one. Check this out! If you have more questions reach out to a qualified professional for your specific scenario.