Many faithful Christians, like you, have stewarded their money and been cared for well by the Lord’s merciful hand. Yet when it’s time to retire, new questions come up: “Will our money last? How much will go to taxes? Can we keep giving generously like we always have?” These questions are no small matter. It’s not as simple as it was while you were earning well and saving 15% of your income for retirement.

Required Minimum Distributions (RMDs) can force you to realize taxable income at the exact time you’re trying to minimize your taxes and maximize your Kingdom impact. These forced distributions from your pre-tax retirement accounts can cause your capital gains tax rate to increase, make your Medicare premiums more expensive, and cause more of your social security to be taxed.

An efficient and thoughtful withdrawal strategy that makes use of QCDs, Roth conversions, Donor Advised Funds, and strategic capital gain and loss harvesting can help you generate sustainable retirement income, keep more in your accounts longer, reduce your lifetime taxes, and actually increase the amount you give back to God’s work and to your heirs. Proverbs 21:5 says “The plans of the diligent lead to profit as surely as haste leads to poverty.” You don’t have to close your eyes and hope that everything works out alright, we can build a plan that works. As a Certified Kingdom Advisor® nothing makes me happier than helping the people of God execute plans that do just that.

Jack and Jill are turning 70 this year. They married young and had humble beginnings but good careers. Jill was a nurse and retired a few years ago when she turned 65 since they wouldn’t need her employers’ health coverage any longer. Jack’s consulting business did really well for the past decade and they were able to save well over that time. They have about $700,000 dollars in taxable savings and another $1,800,000 saved in pre-tax IRA/401(k)s. They put off taking social security as long as possible while their income was high but will have to start that soon. Their Required Minimum Distributions are going to start when they turn 73. They want to continue giving generously to their church and other charities they are passionate about. They’ve always tithed faithfully while living modestly. They were never all about fancy cars or luxury vacations. Even though they’ve done well and have always lived a relatively simple life they’re still concerned about running out of money. It’s a big shift to change from accumulating to decumulating.

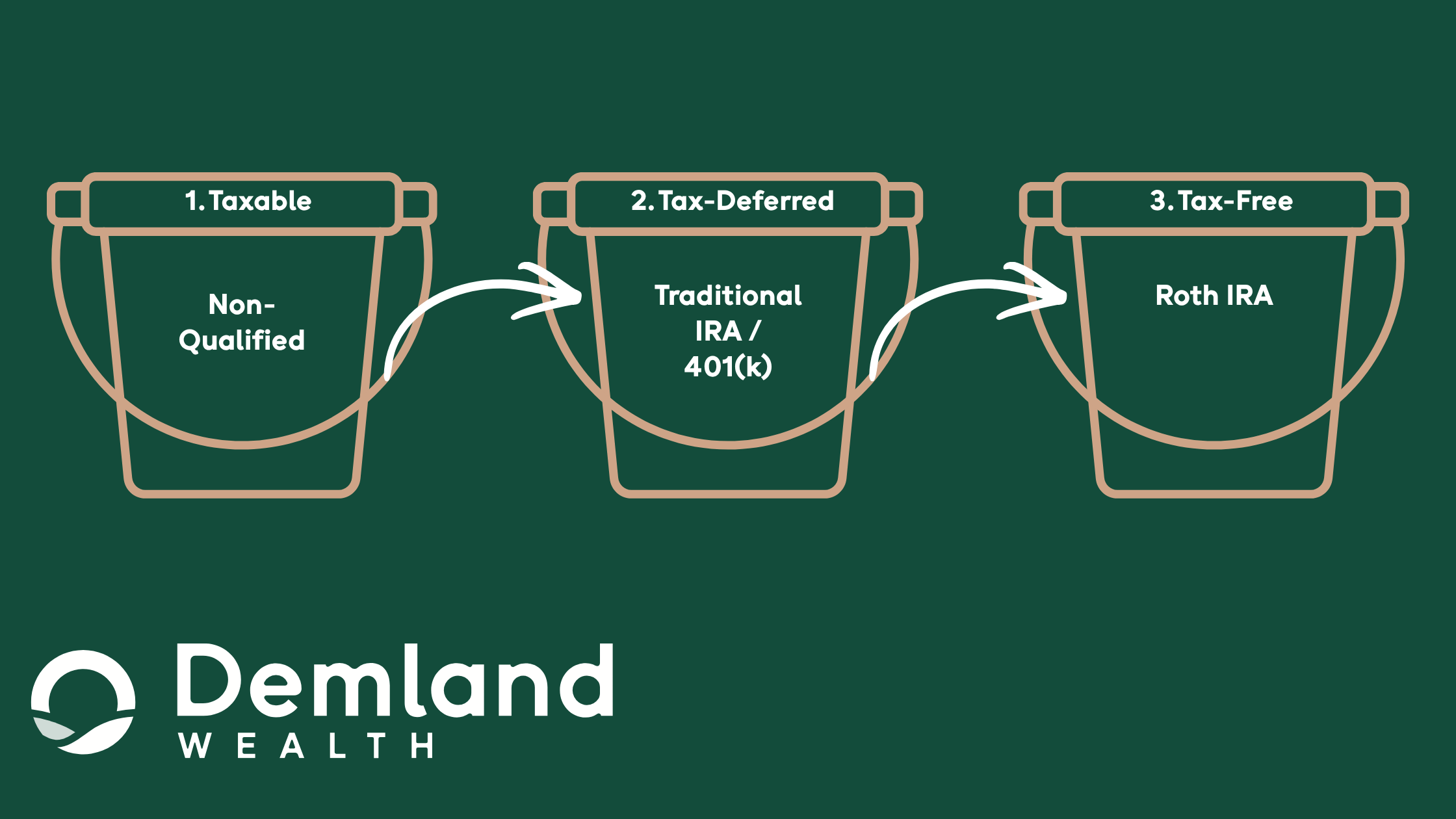

The 3 Buckets That Make Up Your Portfolio

In retirement there are three buckets you can take money out of to fund your retirement: Taxable, Tax-Deferred, and Tax-free.

- Taxable accounts (~$700K): Already-taxed money; withdrawals often qualify for favorable long-term capital gains rates if appreciated (0%, 15%, or 20%).

- Tax-deferred accounts (~$1.8M in IRAs/401(k)s): Future withdrawals taxed as ordinary income; subject to RMDs starting at age 73 (for those born 1951–1959).

- Tax-free accounts (Roth IRAs) Our example couple has zero money in Roths right now, but we can fix that by converting money from tax-deferred accounts strategically. Tax-free accounts are optimal because they add flexibility, certainty, and are the best for your heirs to inherit.

The order of distribution from these accounts matters. Pulling from the wrong bucket first can unnecessarily increase taxes, cause more social security to be taxable, or trigger Medicare IRMAA surcharges. The goal isn’t to empty any one bucket first, but to draw from them in the order that keeps more money growing tax-efficiently for you, your heirs, and the Kingdom.

A Recommended Tax-Efficient Withdrawal Sequencing Strategy

- First satisfy any RMDs that are due. This can be done by using QCDs (Qualified Charitable Distribution) as soon as you reach age 70 1⁄2, even if your RMDs won’t begin until you’re 73. If you retire before RMDs begin, you don’t need to take any money from your pre-tax accounts, but it may make sense to look at doing Roth conversions in Step 3 below.

- Withdraw from taxable accounts after your RMDs are satisfied. Taxable accounts are taxed at capital gains tax rates, which are often lower than ordinary income tax rates. With some efficient planning these can be taxed as low as 0%.

- Next use money from tax-deferred accounts like Traditional IRAs, SEP IRAs, SIMPLE IRAs, and pre-tax 401(k)s. If you’re in sufficiently lower tax-brackets (usually sub 24%) then you are able to “fill up” these tax brackets by funding partial Roth conversions if they are beneficial to you.

- Lastly, take money out of Roth accounts. This preserves tax-free growth for later distributions and any inheritance you plan to leave.

To remain efficient with this it’s extremely important to monitor market returns, your Social Security claiming strategy, healthcare costs, and charitable giving goals. Sustained market growth may offer opportunities to adjust the plan, and market drops can offer other opportunities.

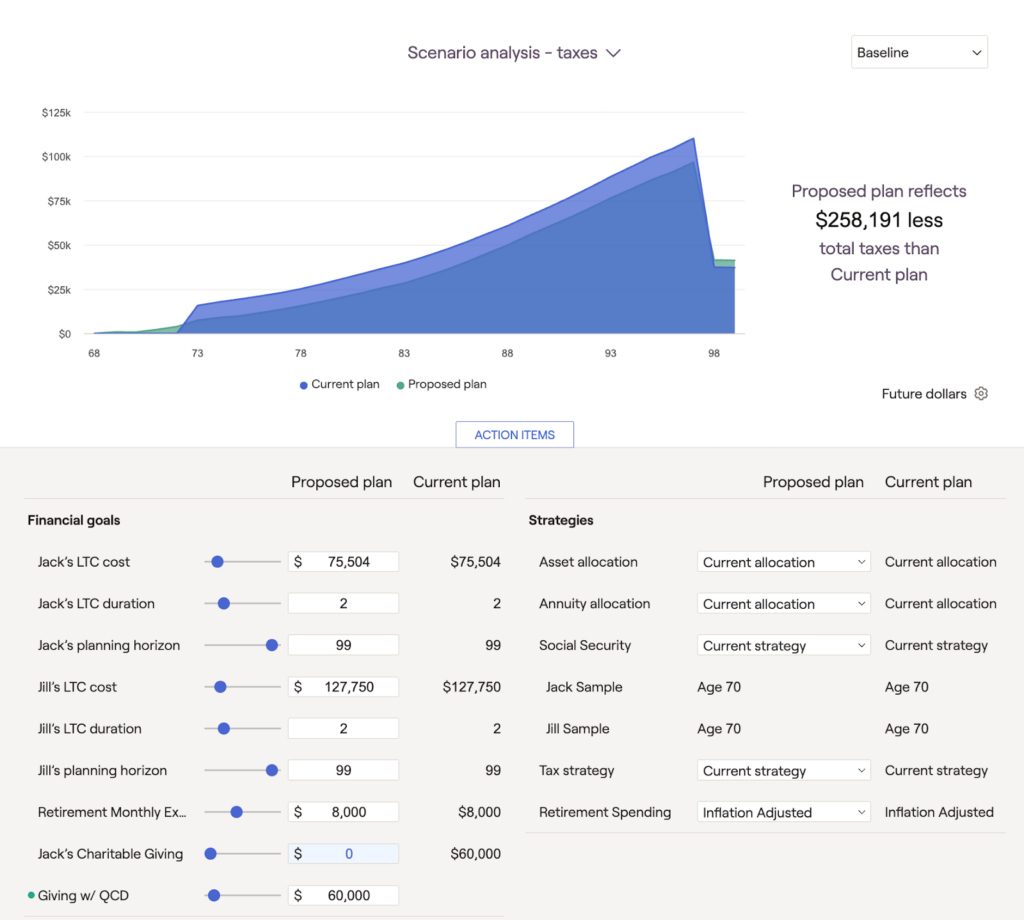

For Jack and Jill, they have all of their investable assets in taxable and tax-deferred accounts. This is common for folks who had high earning years before retirement. The tax-break offered for a current year was too good to ignore, so they saved in tax-deductible accounts like traditional IRAs and 401(k)s. But when RMDs begin they’ll be forced to take out around 90k a year. That amount will keep increasing with market growth and increases in the factor used to determine RMDs. By their 80’s Jack and Jill’s income from RMDs alone will be over 200k a year, in their 90s it keeps creeping up towards 400k a year. That seems like a good problem to have, (render unto Caesar right?), but there’s no reason to pay more taxes than you have to.

Using Qualified Charitable Distributions (QCDs) to give more and grow more

A QCD is a direct transfer from a traditional IRA to a qualified charity available at age 70 1/2 and up. In 2026 up to $111,000 per person annually is eligible to donate via QCD. A QCD satisfies RMDs without increasing your adjusted gross income (AGI) which protects social security taxation and medicare premiums. This also frees up more money to give, because the withdrawn dollars are not taxed. It’s far more efficient than withdrawing the money, paying the tax, and then giving to the charity. If you’re giving anyway, this is a low-effort way to increase your tax-efficiency and generosity. Using QCDs as your primary method of satisfying RMDs and your giving goals simultaneously frees up taxable or other money for living expenses and potentially much lower overall tax exposure.

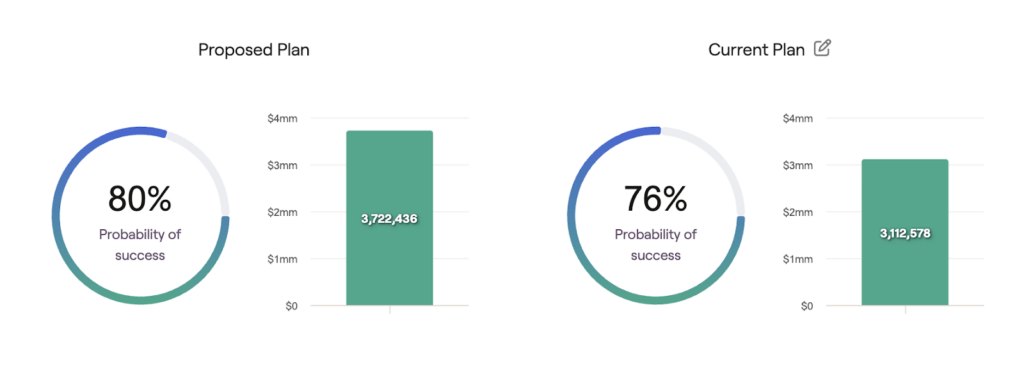

Jack and Jill need about $113,000 for all of their annual expenses (not counting giving and taxes). They want to continue to give 60k a year to their church through retirement. They have enough to do this without running out of money already, but if they switch their giving of that 60k to QCDs they’ll have saved an additional 258k in taxes that they could give away, live off of, or grow for later.

By satisfying their $60k annual giving goal through QCDs instead of after-tax dollars, Jack and Jill avoid roughly 24–37% ordinary income tax on those distributions—freeing up an estimated $258k over their lifetime that can be redirected to additional giving, living expenses, or tax-free growth.

If they really want to supercharge this plan they can incorporate giving to a Donor-Advised Fund with Roth conversions, which is something we’ll cover later. Many of our clients in this position discover they can give even more generously with confidence in retirement than during peak earning years. When you implement these strategies you’re not just reducing your tax bill so you have more money. You’re causing more of the resources God entrusted to you to flow straight into His work rather than to the IRS.

2 Corinthians 9:7 “God loves a cheerful giver”

Common Traps to Avoid

The primary takeaway from this is that taking a full RMD as cash and then donating it is often an exercise in paying unnecessary taxes. From the illustration above it just amounts to a donation to the IRS rather than your church or charity you care about. It’s a very easy strategy to implement. The distribution in a QCD must go straight from your IRA to the charity to count. It’s important to reconcile these QCDs when you get your 1099-R for your IRA when filing your taxes. Your custodian will issue a 1099-R but you must report the QCD correctly on your return so it’s excluded from your income. I implore you to do this and tell the rest of your over 70 church family about it!

Another pitfall is ignoring tax-bracket management and coordination with Social Security. Every distribution from a pre-tax retirement account is going to cause ordinary income taxes. Tax laws change constantly. Some precision is required when figuring out distributions. Remember that increases in ordinary income can impact your capital gains tax brackets, Medicare premium surcharges, and the taxable amount of your social security. Even a modest increase in ordinary income can make up to 85% of your Social Security taxable and trigger IRMAA surcharges that raise your Part B & D premiums by thousands each year.

Jack and Jill did a great job of saving for retirement. They were generous their whole lives. Now that they are retiring, with periodic review and implementation of these tax strategies they have an even more positive kingdom impact and security in their retirement income plan.

Conclusion

Diligent planning with the right withdrawal sequence and QCDs lets you retire confidently, steward your resources well, and bless the Kingdom more abundantly. It’s worth the effort to be able to live better, give more, and grow well.

Always remember Matthew 6:19-21 “Do not store up for yourselves treasures on earth…but store up for yourselves treasures in heaven.” and the freedom that we have in Christ to live for Him and His Kingdom.

If you’re retiring or recently retired and have more than $1M in investable assets and want a personalized tax-efficient income and giving plan modeled for you, book a call today. Our team of CFP® Professionals, CKA®, and EA would be honored to help you align your finances with your faith and values.